972-492-1370

Trends and Innovations

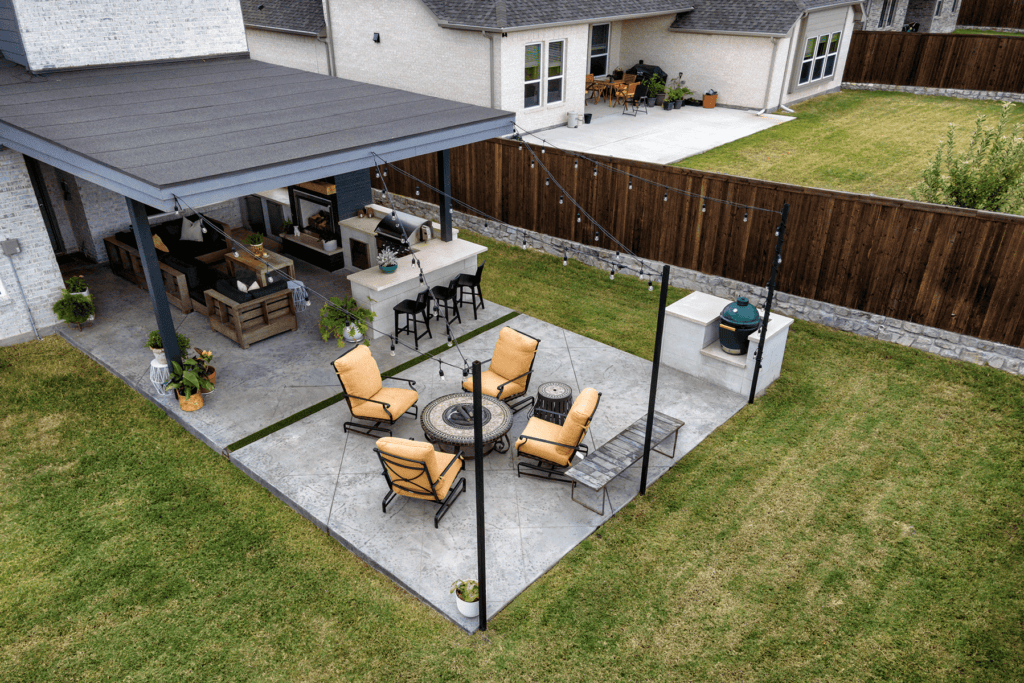

How Contractor Insurance Protects Your Home: What Every Homeowner Should Know Before Hiring

When you invite a contractor into your home, you’re placing a tremendous amount of trust in them, trust in their workmanship, their professionalism, and their ability to protect your property. At Southwest Fence & Deck, we take that responsibility seriously. And one of the most important, yet least understood, parts of that responsibility is insurance.

Most homeowners focus on design, materials, or price. But the truth is simple: Even the best-built outdoor space starts with the right insurance behind it.

To help break down what really matters, we sat down with our longtime insurance broker, Richard Phillips, who has supported us for more than two decades. His insights reveal what homeowners don’t see behind the scenes and why the right insurance coverage is just as important as the craftsmanship you hire us for. Watch the full video here.

Table of contents

The Hidden Risks in Contractor Insurance That Homeowners Often Miss

A Certificate of Insurance can give homeowners the impression that everything is covered, but Richard explained that this document only tells part of the story. A COI shows that a policy exists, although it does not reveal the specific activities that the policy covers or whether subcontractors are properly insured. Many of the risks that matter most are hidden in the details.

“Just because a contractor hands you a COI doesn’t mean they’re covered for the work they’re actually doing.” – Richard Philips, Insurance Broker.

At Southwest Fence & Deck, we work hard to identify these gaps before they affect homeowners. We review details that many people have never been taught to look for, and we make sure our teams and vehicles are insured in ways that align with the work being done.

Here are a few of the risks homeowners should be aware of when evaluating contractor insurance:

Common homeowner risks and what they mean

- A COI does not guarantee proper coverage: This document confirms a policy exists, although it does not specify whether the contractor is insured for the type of work you are hiring them to do.

- Subcontractors may be uninsured for worker injuries: Without workers’ compensation, an injured worker can trigger claims that involve the contractor and the homeowner.

- Commercial vehicles require listed drivers to be valid: Coverage only applies if the specific drivers and vehicles are listed on the commercial auto policy.

- Certain project activities may fall outside a contractor’s policy: A contractor may be insured for one skill but performing another on your property, which can leave gaps in protection.

These are examples of details we verify internally so that homeowners do not have to worry about them. We see insurance as part of our commitment to providing reliable service and dependable protection.

Why Hiring a Contractor With In-House Employees Safeguards Your Project

In our industry, there is a clear difference between contractors who employ in-house crews and those who rely almost entirely on independent subcontractors.

Richard often refers to the latter as “paper contractors” because they manage paperwork rather than the actual work on site. They may not know the people arriving at a homeowner’s property, and they may never verify the insurance those subs carry.

Southwest Fence & Deck operates with an in-house team that checks in with us every morning. We know who is representing our company, how they have been trained, and what coverage they carry. This daily connection ensures consistency in skill, attitude, and accountability. It is part of how we manage quality and maintain a safe work environment.

Richard described the consequences of relying on unknown subcontractors in a straightforward way.

“If a contractor doesn’t know who’s actually on your job site, that creates a problem.” – Richard Phillips.

Subcontractors without proper insurance can leave costly gaps. When a worker is injured, a gas line is hit, or property is damaged, those events can lead to claims that impact the homeowner. By investing in a stable workforce, we reduce these variables and create a safer and more dependable experience for the families we serve.

How Contractor Insurance Details Protect Your Home and Project

Insurance coverage is built through a combination of policy limits, endorsements, and active management. Richard emphasized that endorsements often determine whether a claim is accepted or rejected. These details matter because outdoor construction involves many disciplines, including carpentry, concrete, metalwork, utilities, and electrical components.

Endorsements such as additional insured status ensure that if a subcontractor is involved, their policy extends protection to Southwest Fence & Deck and the homeowner. A waiver of subrogation prevents the insurer from seeking repayment from the homeowner after settling a claim. Primary and noncontributory language ensures that the contractor’s coverage responds before the homeowner’s.

These are not technicalities. They are protections that we rely on every time we build an outdoor space. Richard has managed these details for us for many years, and Jamie expressed how much that support matters to our team.

“One mistake could cost everything, and Richard makes sure we’re protected.”

Our work involves creativity, engineering, and craftsmanship. Insurance is what keeps that work secure so that homeowners can enjoy their spaces with confidence.

What Homeowners Should Review Before Hiring a Contractor

Homeowners do not need to be insurance experts to make wise decisions about who to hire. Richard recommends one simple step that most people overlook. Call your home or auto insurance agent and ask them to review the contractor’s certificate of insurance. Your agent already understands your policy and can help determine whether the contractor’s coverage is appropriate.

Richard also suggested asking whether the contractor handles commercial projects. Companies that do commercial work are often required to meet rigorous insurance standards. Passing that level of scrutiny is a sign that the contractor maintains strong, consistent coverage in every part of their business.

Contractor stability is another valuable indicator. Insurance history shows whether a contractor maintains relationships with the same agent and insurer, or changes frequently. Consistency usually reflects responsibility and long-term planning.

Practical steps homeowners can take

• Have your insurance agent review the contractor’s COI

Your agent can identify missing coverages or potential risks based on your property.

• Ask whether the contractor uses in-house employees

In-house teams offer predictable training, insurance, and oversight.

• Request information about workers compensation and liability limits

These should align with the size and complexity of your project.

• Confirm that any subcontractors are properly insured

Every person on your property should be protected under the right policy.

• Look for a contractor with stable insurance history

Long-term coverage demonstrates accountability and reliability.

Conclusion

At Southwest Fence & Deck, we believe that great outdoor spaces begin with careful planning, skilled craftsmanship, and dependable protection.

Insurance is part of how we safeguard your investment and honor the trust you place in us. When your contractor carries the right coverage, you gain peace of mind along with a beautifully built project.

Categories

Recent Post

Patio Covers vs Pergolas: Which Shade Structure Fits Your Home Best?

March 2, 2026 / 0 Comments

Custom Wood Vs Metal Fences: Choosing the Right Style for Your Home

January 27, 2026 / 0 Comments